There is a loose association between stock market rallies (w little fundamental foundation) and Gold, Silver, Stock market and currency manipulation being perpetrated by variuos combinations of banks (e.g JP Morgan and HSBC), central banks, other govt entities, and perhaps non-bank wall street financial firms. This week the CFTC (Commodity Futures Trading Commission) is holding hearings regarding past market manipulations and possible future position limits on futures contracts in the precious metals. I've discussed this before and provided links in previous posts. There are, IMO, important new developements and info around these hearings which I believe to be important beyond just those who are investing in gold and silver. Gold and silver price suppression helps central banks maintain the illusion of value of the paper money their printing presses spew forth daily, and allows parasitic bankers and other colluding Wall Street financial firms to keep taking their huge cuts, w/o risk or even any work, while sitting on their gold plated toilet seats in their corner offices, laughing at those us who do actual work (you don't have to include me in that group).

Here is an account of market manipulation by London metal trader Andrew Maguire, all signaled and communicated to the CFTC in advance of the event. Very credible stuff, IMO.

http://www.gata.org/node/8466

Days after his name came out, he was involved in a hit and run accident in London. The details are not all in but Intimidation or assasination attempt certainly seem within the realm of possibilty

http://www.gata.org/node/8482

A second whistleblower-

by

Bix Weir

I've been watching the CFTC hearing over and over again to pick up tid-bits and came across something that nobody has been discussing.

A SECOND SHOOTER! (I mean whistle blower :)

He is revealed by Bart Chilton at 51:30 minutes into the meeting:

http://www.capitolconnection.net/capcon/cftc/032510/cftc-archive-wmv.htm

"Over the last couple of years, and before you (Sherrod) were in this position also, I've been given individual emails...some that actually forecast that the market in silver and in gold will PLUMMET....and it's going to happen and they'll say 'Look at 9 o'clock'. Paul Kaplan, Andrew Mcguire and others have said this sort of thing."

It isn't until much later in the hearing that Bill Murphy exposes Andrew Mcguire as his whistleblower so clearly Bart Chilton knew what was going to be exposed before hand which validates those "crazy tinfoil hatters" claim of a credible whistle blower.

But what about that first guy that Commissioner Chilton spoke of who knew what was going to happen on a gold/silver slam before it did. Who is he?

Well it turns out the second whistleblower is no slouch when it comes to credibility.

"Paul D. Kaplan, Ph.D., CFA is vice president of quantitative research for Morningstar, responsible for the quantitative methodologies behind Morningstar's fund analysis, indexes, advisor tools, and other services. He conducts research on style analysis, performance and risk measurement, asset allocation, retirement income planning, portfolio construction, index methodologies, and alternative investments. Kaplan led the development of quantitative methodologies behind the Morningstar RatingTM for funds, the Morningstar Style BoxTM, and the Morningstar family of indexes. He has served as chief investment officer of Morningstar Associates, LLC, a registered investment advisor and wholly owned subsidiary of Morningstar, Inc., where he developed and managed the investment methodology for Morningstar's retirement planning and advice services."

http://secure.imn.org/web_confe/pop_bio.cfm?personid=KAPLI60601

If this is the "Paul Kaplan" that Bart Chilton is referring too you have an "insiders-insider" turning states evidence in this massive manipulation scam.

Only time will tell because the CFTC is clearly waiting for the right moment to put the hammer down.

I think that moment may happen... ANY MOMENT!!!

**********************************************************************

How to corner the gold market?

http://www.gata.org/node/8486

********************************************************************

by

Bix Weir

I've been watching the CFTC hearing over and over again to pick up tid-bits and came across something that nobody has been discussing.

A SECOND SHOOTER! (I mean whistle blower :)

He is revealed by Bart Chilton at 51:30 minutes into the meeting:

http://www.capitolconnection.net/capcon/cftc/032510/cftc-archive-wmv.htm

"Over the last couple of years, and before you (Sherrod) were in this position also, I've been given individual emails...some that actually forecast that the market in silver and in gold will PLUMMET....and it's going to happen and they'll say 'Look at 9 o'clock'. Paul Kaplan, Andrew Mcguire and others have said this sort of thing."

It isn't until much later in the hearing that Bill Murphy exposes Andrew Mcguire as his whistleblower so clearly Bart Chilton knew what was going to be exposed before hand which validates those "crazy tinfoil hatters" claim of a credible whistle blower.

But what about that first guy that Commissioner Chilton spoke of who knew what was going to happen on a gold/silver slam before it did. Who is he?

Well it turns out the second whistleblower is no slouch when it comes to credibility.

"Paul D. Kaplan, Ph.D., CFA is vice president of quantitative research for Morningstar, responsible for the quantitative methodologies behind Morningstar's fund analysis, indexes, advisor tools, and other services. He conducts research on style analysis, performance and risk measurement, asset allocation, retirement income planning, portfolio construction, index methodologies, and alternative investments. Kaplan led the development of quantitative methodologies behind the Morningstar RatingTM for funds, the Morningstar Style BoxTM, and the Morningstar family of indexes. He has served as chief investment officer of Morningstar Associates, LLC, a registered investment advisor and wholly owned subsidiary of Morningstar, Inc., where he developed and managed the investment methodology for Morningstar's retirement planning and advice services."

http://secure.imn.org/web_confe/pop_bio.cfm?personid=KAPLI60601

If this is the "Paul Kaplan" that Bart Chilton is referring too you have an "insiders-insider" turning states evidence in this massive manipulation scam.

Only time will tell because the CFTC is clearly waiting for the right moment to put the hammer down.

I think that moment may happen... ANY MOMENT!!!

*********************************************************************************

Answers to a market manipulation sceptic

http://www.gata.org/node/8488

Wednesday, March 31, 2010

US stock market returns - what is in store?

By Dr. Prieur du Plessis

Surging stock markets since the lows of March 2009 have caught most investors by surprise, especially as new pieces of the economics puzzle are not always rosy and do not quite seem to support an overly bullish case. In short, investors are increasingly struggling to make sense of the most likely direction of stock prices.

Are we perhaps nearing the end of a cyclical bull phase in a structural bull market? Or will strong earnings growth ensure the longevity of the bull? Or is a "muddle-through" trading range in store? It seems to be a case of so many pundits, so many views.

It is one thing to trade the market's rallies and corrections, but this is easier said than done, with not many people actually getting it right with any degree of consistency. Others are of the opinion that the recipe for creating wealth is simply to follow the patient approach, saying that "it's time in the market, not timing the market" that counts. But "buy-and-hold" investors in the S&P 500 Index are still 25.5% down from the levels of 10 years ago, the Dow Jones Industrial Index a similar 23.5% lower and the Nasdaq Composite Index a massive 52.5% under water.

This gives rise to the all-important question: does one's entry level into the market, i.e. the valuation of the market at the time of investing, make a significant difference to subsequent investment returns?

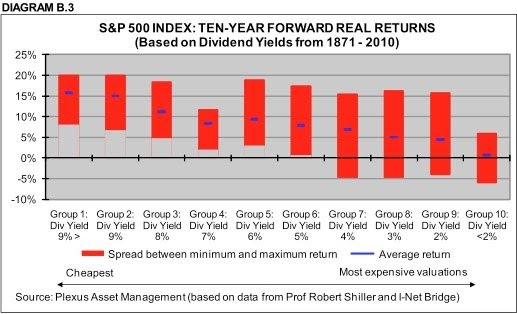

In an attempt to cast light on this issue, my colleagues at Plexus Asset Management have updated a previous multi-year comparison of the price-earnings (PE) ratios of the S&P 500 Index (as a measure of stock valuations) and the forward real returns (considering total returns, i.e. capital movements plus dividends). The study covered the period from 1871 to March 2010 and used the S&P 500 (and its predecessors prior to 1957). In essence, PEs based on rolling average ten-year earnings were calculated and used together with ten-year forward real returns.

In the first analysis the PEs and the corresponding ten-year forward real returns were grouped in five quintiles (i.e. 20% intervals) (Diagram A.1).

The cheapest quintile had an average PE of 7.7 with an average ten-year forward real return of 11.4% per annum, whereas the most expensive quintile had an average PE of 23.4 with an average ten-year forward real return of only 3.8% per annum.

This analysis clearly shows the strong long-term relationship between real returns and the level of valuation at which the investment was made.

The study was then repeated with the PEs divided into smaller groups, i.e. deciles or 10% intervals (see Diagrams A.2 and A.3).

This analysis strongly confirms the downward trend of the average ten-year forward real returns from the cheapest grouping (PEs of less than six) to the most expensive grouping (PEs of more than 21). The second study also shows that any investment at PEs of less than 12 always had positive ten-year real returns, while investments at PE ratios of 12 and higher experienced negative real returns at some stage.

This analysis strongly confirms the downward trend of the average ten-year forward real returns from the cheapest grouping (PEs of less than six) to the most expensive grouping (PEs of more than 21). The second study also shows that any investment at PEs of less than 12 always had positive ten-year real returns, while investments at PE ratios of 12 and higher experienced negative real returns at some stage.

A third observation from this analysis is that the ten-year forward real returns of investments made at PEs between 12 and 17 had the biggest spread between minimum and maximum returns and were therefore more volatile and less predictable.

As a further refinement, holding periods of one, three, five and 20 years were also analyzed. The research results (not reported in this article) for the one-year period showed a poor relationship with expected returns, but the findings for all the other periods were consistent with the findings for the ten-year periods.

Although the above analysis represents an update to and extension of an earlier study by Jeremy Grantham's GMO, it was also considered appropriate to replicate the study using dividend yields rather than PEs as valuation yardstick. The results are reported in Diagrams B.1, B.2 and B.3 and, as can be expected, are very similar to those based on PEs.

Based on the above research findings, with the S&P 500 Index's current ten-year normalized PE of 20.3 and ten-year normalized dividend yield of 2.1%, investors should be aware of the fact that the market is by historical standards expensive. As far as the market in general is concerned, this argues for unexciting long-term returns, possibly a "muddle-through" trading range for quite a number of years to come.

Based on the above research findings, with the S&P 500 Index's current ten-year normalized PE of 20.3 and ten-year normalized dividend yield of 2.1%, investors should be aware of the fact that the market is by historical standards expensive. As far as the market in general is concerned, this argues for unexciting long-term returns, possibly a "muddle-through" trading range for quite a number of years to come.

Although the research results offer no guidance as to calling market tops and bottoms, they do indicate that it would not be consistent with the findings to bank on above-average returns based on the current ten-year normalized valuation levels. As a matter of fact, there is a distinct possibility of some negative returns off current price levels.

Surging stock markets since the lows of March 2009 have caught most investors by surprise, especially as new pieces of the economics puzzle are not always rosy and do not quite seem to support an overly bullish case. In short, investors are increasingly struggling to make sense of the most likely direction of stock prices.

Are we perhaps nearing the end of a cyclical bull phase in a structural bull market? Or will strong earnings growth ensure the longevity of the bull? Or is a "muddle-through" trading range in store? It seems to be a case of so many pundits, so many views.

It is one thing to trade the market's rallies and corrections, but this is easier said than done, with not many people actually getting it right with any degree of consistency. Others are of the opinion that the recipe for creating wealth is simply to follow the patient approach, saying that "it's time in the market, not timing the market" that counts. But "buy-and-hold" investors in the S&P 500 Index are still 25.5% down from the levels of 10 years ago, the Dow Jones Industrial Index a similar 23.5% lower and the Nasdaq Composite Index a massive 52.5% under water.

This gives rise to the all-important question: does one's entry level into the market, i.e. the valuation of the market at the time of investing, make a significant difference to subsequent investment returns?

In an attempt to cast light on this issue, my colleagues at Plexus Asset Management have updated a previous multi-year comparison of the price-earnings (PE) ratios of the S&P 500 Index (as a measure of stock valuations) and the forward real returns (considering total returns, i.e. capital movements plus dividends). The study covered the period from 1871 to March 2010 and used the S&P 500 (and its predecessors prior to 1957). In essence, PEs based on rolling average ten-year earnings were calculated and used together with ten-year forward real returns.

In the first analysis the PEs and the corresponding ten-year forward real returns were grouped in five quintiles (i.e. 20% intervals) (Diagram A.1).

The cheapest quintile had an average PE of 7.7 with an average ten-year forward real return of 11.4% per annum, whereas the most expensive quintile had an average PE of 23.4 with an average ten-year forward real return of only 3.8% per annum.

This analysis clearly shows the strong long-term relationship between real returns and the level of valuation at which the investment was made.

The study was then repeated with the PEs divided into smaller groups, i.e. deciles or 10% intervals (see Diagrams A.2 and A.3).

A third observation from this analysis is that the ten-year forward real returns of investments made at PEs between 12 and 17 had the biggest spread between minimum and maximum returns and were therefore more volatile and less predictable.

As a further refinement, holding periods of one, three, five and 20 years were also analyzed. The research results (not reported in this article) for the one-year period showed a poor relationship with expected returns, but the findings for all the other periods were consistent with the findings for the ten-year periods.

Although the above analysis represents an update to and extension of an earlier study by Jeremy Grantham's GMO, it was also considered appropriate to replicate the study using dividend yields rather than PEs as valuation yardstick. The results are reported in Diagrams B.1, B.2 and B.3 and, as can be expected, are very similar to those based on PEs.

Although the research results offer no guidance as to calling market tops and bottoms, they do indicate that it would not be consistent with the findings to bank on above-average returns based on the current ten-year normalized valuation levels. As a matter of fact, there is a distinct possibility of some negative returns off current price levels.

Tuesday, March 30, 2010

global (not) warming, CO2, the death of truth, and Ocean acidification

A while back, I was debating AGW (anthropogenic global warming) with Randy McDonnell, and brought up the ocean acidification issue. At the time I didn't know anything about it and it was a little "off topic", so I swept it under the rug at the time. Now, as AGW is increasingly less relevant, due to intellectual fraud amongst many of its principal investigators, and clear lack of scientific evidence, the "War on Carbon" is setting its sights on "ocean acidification", which is just more BS. So, this one's for you Randy!

The Next Big Thing

In environmental politics, it'll be 'ocean acidification'

Written By: James Taylor

Publication date: 03/29/2010

Publisher: The Heartland Institute

Remember you read it here first: The Next Big Thing in environmental politics will be “ocean acidification.”

That was assured this month when the U.S. Environmental Protection Agency caved in to to the bullying tactics of enviro pressure groups, and proclaimed that EPA regulators will use the Clean Water Act to remedy a problem that doesn’t exist.

The EPA’s decision came in response to a lawsuit alleging the agency should have required the state of Washington to designate its marine waters as impaired by rising acidity. But in doing so, the EPA ignored sound science and did a disservice to Washington citizens. read the rest of the article

****************************************************************************

Global Warming Benefits Outweigh Harms

Written By: Walter Cunningham

Published In: Environment & Climate News > April 2010

Publication date: 03/09/2010

Publisher: The Heartland Institute

--------------------------------------------------------------------------------

[Editor’s note: This is the third article in a series by scientist/astronaut Walter Cunningham, who was the pilot of the Apollo 7 space mission and possesses a master’s degree in physics. Cunningham has served on the Advisory Board for the National Renewable Energy Laboratory.]

Without the greenhouse effect to keep our world warm, the planet would have an average temperature of minus 18 degrees Celsius. Because we do have it, the temperature is a comfortable plus 15 degrees Celsius.

Other inconvenient facts ignored by the activists: Carbon dioxide is a non-polluting gas that is essential for plant photosynthesis. Higher concentrations of CO2 in the atmosphere produce bigger crop harvests and larger and healthier forests--results environmentalists used to like.

There are legitimate reasons to restrict emissions of pollutants into the atmosphere. Recycling makes sense and protecting the environment is good for everyone. But we should not fool ourselves into thinking we can change the temperature of the Earth by doing these things. more

*******************************************************************

Jesse Ventura puts the SMACKDOWN on the AGW conspiracy

http://www.youtube.com/watch?v=sm54OTiTR6E&feature=PlayList&p=FABB5A22DCCF564A&playnext=1&playnext_from=PL&index=35

**************************************************************************************

California Warming Law will Kill Jobs, Concludes Nonpartisan Report

James M. Taylor - March 11, 2010

Proponents of California’s greenhouse gas reduction law used flawed economic models to assert the bill will create more jobs than it kills, concludes ...http://www.heartland.org/environmentandclimate-news.org/article/27220/California_Warming_Law_will_Kill_Jobs_Concludes_Nonpartisan_Report_.html

**********************************************************************

And finally, I'm copying and pasting this entire article covering intellectual and moral fraud, not just in the AGW camp, but everywhere in the US right now. I thought it was an important piece by a respected journalist, and I urge everyone to read the whole thing.

Good-Bye: Truth Has Fallen and Taken Liberty With It

by Paul Craig Roberts

There was a time when the pen was mightier than the sword. That was a time when people believed in truth and regarded truth as an independent power and not as an auxiliary for government, class, race, ideological, personal, or financial interest.

Today Americans are ruled by propaganda. Americans have little regard for truth, little access to it, and little ability to recognize it.

Truth is an unwelcome entity. It is disturbing. It is off limits. Those who speak it run the risk of being branded “anti-American,” “anti-semite” or “conspiracy theorist.”

Truth is an inconvenience for government and for the interest groups whose campaign contributions control government.

Truth is an inconvenience for prosecutors who want convictions, not the discovery of innocence or guilt.

Truth is inconvenient for ideologues.

Today many whose goal once was the discovery of truth are now paid handsomely to hide it. “Free market economists” are paid to sell offshoring to the American people. High-productivity, high value-added American jobs are denigrated as dirty, old industrial jobs. Relicts from long ago, we are best shed of them. Their place has been taken by “the New Economy,” a mythical economy that allegedly consists of high-tech white collar jobs in which Americans innovate and finance activities that occur offshore. All Americans need in order to participate in this “new economy” are finance degrees from Ivy League universities, and then they will work on Wall Street at million dollar jobs.

Economists who were once respectable took money to contribute to this myth of “the New Economy.”

And not only economists sell their souls for filthy lucre. Recently we have had reports of medical doctors who, for money, have published in peer-reviewed journals concocted “studies” that hype this or that new medicine produced by pharmaceutical companies that paid for the “studies.”

The Council of Europe is investigating the drug companies’ role in hyping a false swine flu pandemic in order to gain billions of dollars in sales of the vaccine.

The media helped the US military hype its recent Marja offensive in Afghanistan, describing Marja as a city of 80,000 under Taliban control. It turns out that Marja is not urban but a collection of village farms.

And there is the global warming scandal, in which NGOs. the UN, and the nuclear industry colluded in concocting a doomsday scenario in order to create profit in pollution.

Wherever one looks, truth has fallen to money.

Wherever money is insufficient to bury the truth, ignorance, propaganda, and short memories finish the job.

I remember when, following CIA director William Colby’s testimony before the Church Committee in the mid-1970s, presidents Gerald Ford and Ronald Reagan issued executive orders preventing the CIA and U.S. black-op groups from assassinating foreign leaders. In 2010 the US Congress was told by Dennis Blair, head of national intelligence, that the US now assassinates its own citizens in addition to foreign leaders.

When Blair told the House Intelligence Committee that US citizens no longer needed to be arrested, charged, tried, and convicted of a capital crime, just murdered on suspicion alone of being a “threat,” he wasn’t impeached. No investigation pursued. Nothing happened. There was no Church Committee. In the mid-1970s the CIA got into trouble for plots to kill Castro. Today it is American citizens who are on the hit list. Whatever objections there might be don’t carry any weight. No one in government is in any trouble over the assassination of U.S. citizens by the U.S. government.

As an economist, I am astonished that the American economics profession has no awareness whatsoever that the U.S. economy has been destroyed by the offshoring of U.S. GDP to overseas countries. U.S. corporations, in pursuit of absolute advantage or lowest labor costs and maximum CEO “performance bonuses,” have moved the production of goods and services marketed to Americans to China, India, and elsewhere abroad. When I read economists describe offshoring as free trade based on comparative advantage, I realize that there is no intelligence or integrity in the American economics profession.

Intelligence and integrity have been purchased by money. The transnational or global U.S. corporations pay multi-million dollar compensation packages to top managers, who achieve these “performance awards” by replacing U.S. labor with foreign labor. While Washington worries about “the Muslim threat,” Wall Street, U.S. corporations and “free market” shills destroy the U.S. economy and the prospects of tens of millions of Americans.

Americans, or most of them, have proved to be putty in the hands of the police state.

Americans have bought into the government’s claim that security requires the suspension of civil liberties and accountable government. Astonishingly, Americans, or most of them, believe that civil liberties, such as habeas corpus and due process, protect “terrorists,” and not themselves. Many also believe that the Constitution is a tired old document that prevents government from exercising the kind of police state powers necessary to keep Americans safe and free.

Most Americans are unlikely to hear from anyone who would tell them any different.

I was associate editor and columnist for the Wall Street Journal. I was Business Week’s first outside columnist, a position I held for 15 years. I was columnist for a decade for Scripps Howard News Service, carried in 300 newspapers. I was a columnist for the Washington Times and for newspapers in France and Italy and for a magazine in Germany. I was a contributor to the New York Times and a regular feature in the Los Angeles Times. Today I cannot publish in, or appear on, the American “mainstream media.”

For the last six years I have been banned from the “mainstream media.” My last column in the New York Times appeared in January, 2004, coauthored with Democratic U.S. Senator Charles Schumer representing New York. We addressed the offshoring of U.S. jobs. Our op-ed article produced a conference at the Brookings Institution in Washington, D.C. and live coverage by C-Span. A debate was launched. No such thing could happen today.

For years I was a mainstay at the Washington Times, producing credibility for the Moony newspaper as a Business Week columnist, former Wall Street Journal editor, and former Assistant Secretary of the U.S. Treasury. But when I began criticizing Bush’s wars of aggression, the order came down to Mary Lou Forbes to cancel my column.

The American corporate media does not serve the truth. It serves the government and the interest groups that empower the government.

America’s fate was sealed when the public and the anti-war movement bought the government’s 9/11 conspiracy theory. The government’s account of 9/11 is contradicted by much evidence. Nevertheless, this defining event of our time, which has launched the US on interminable wars of aggression and a domestic police state, is a taboo topic for investigation in the media. It is pointless to complain of war and a police state when one accepts the premise upon which they are based.

These trillion dollar wars have created financing problems for Washington’s deficits and threaten the U.S. dollar’s role as world reserve currency. The wars and the pressure that the budget deficits put on the dollar’s value have put Social Security and Medicare on the chopping block. Former Goldman Sachs chairman and U.S. Treasury Secretary Hank Paulson is after these protections for the elderly. Fed chairman Bernanke is also after them. The Republicans are after them as well. These protections are called “entitlements” as if they are some sort of welfare that people have not paid for in payroll taxes all their working lives.

With over 21 per cent unemployment as measured by the methodology of 1980, with American jobs, GDP, and technology having been given to China and India, with war being Washington’s greatest commitment, with the dollar over-burdened with debt, with civil liberty sacrificed to the “war on terror,” the liberty and prosperity of the American people have been thrown into the trash bin of history.

The militarism of the U.S. and Israeli states, and Wall Street and corporate greed, will now run their course. As the pen is censored and its might extinguished, I am signing off.

Paul Craig Roberts was an editor of the Wall Street Journal and an Assistant Secretary of the U.S. Treasury. His latest book, HOW THE ECONOMY WAS LOST, has just been published by CounterPunch/AK Press. He can be reached at: PaulCraigRoberts@yahoo.com

The Next Big Thing

In environmental politics, it'll be 'ocean acidification'

Written By: James Taylor

Publication date: 03/29/2010

Publisher: The Heartland Institute

Remember you read it here first: The Next Big Thing in environmental politics will be “ocean acidification.”

That was assured this month when the U.S. Environmental Protection Agency caved in to to the bullying tactics of enviro pressure groups, and proclaimed that EPA regulators will use the Clean Water Act to remedy a problem that doesn’t exist.

The EPA’s decision came in response to a lawsuit alleging the agency should have required the state of Washington to designate its marine waters as impaired by rising acidity. But in doing so, the EPA ignored sound science and did a disservice to Washington citizens. read the rest of the article

****************************************************************************

Global Warming Benefits Outweigh Harms

Written By: Walter Cunningham

Published In: Environment & Climate News > April 2010

Publication date: 03/09/2010

Publisher: The Heartland Institute

--------------------------------------------------------------------------------

[Editor’s note: This is the third article in a series by scientist/astronaut Walter Cunningham, who was the pilot of the Apollo 7 space mission and possesses a master’s degree in physics. Cunningham has served on the Advisory Board for the National Renewable Energy Laboratory.]

Without the greenhouse effect to keep our world warm, the planet would have an average temperature of minus 18 degrees Celsius. Because we do have it, the temperature is a comfortable plus 15 degrees Celsius.

Other inconvenient facts ignored by the activists: Carbon dioxide is a non-polluting gas that is essential for plant photosynthesis. Higher concentrations of CO2 in the atmosphere produce bigger crop harvests and larger and healthier forests--results environmentalists used to like.

There are legitimate reasons to restrict emissions of pollutants into the atmosphere. Recycling makes sense and protecting the environment is good for everyone. But we should not fool ourselves into thinking we can change the temperature of the Earth by doing these things. more

*******************************************************************

Jesse Ventura puts the SMACKDOWN on the AGW conspiracy

http://www.youtube.com/watch?v=sm54OTiTR6E&feature=PlayList&p=FABB5A22DCCF564A&playnext=1&playnext_from=PL&index=35

**************************************************************************************

California Warming Law will Kill Jobs, Concludes Nonpartisan Report

James M. Taylor - March 11, 2010

Proponents of California’s greenhouse gas reduction law used flawed economic models to assert the bill will create more jobs than it kills, concludes ...http://www.heartland.org/environmentandclimate-news.org/article/27220/California_Warming_Law_will_Kill_Jobs_Concludes_Nonpartisan_Report_.html

**********************************************************************

And finally, I'm copying and pasting this entire article covering intellectual and moral fraud, not just in the AGW camp, but everywhere in the US right now. I thought it was an important piece by a respected journalist, and I urge everyone to read the whole thing.

Good-Bye: Truth Has Fallen and Taken Liberty With It

by Paul Craig Roberts

There was a time when the pen was mightier than the sword. That was a time when people believed in truth and regarded truth as an independent power and not as an auxiliary for government, class, race, ideological, personal, or financial interest.

Today Americans are ruled by propaganda. Americans have little regard for truth, little access to it, and little ability to recognize it.

Truth is an unwelcome entity. It is disturbing. It is off limits. Those who speak it run the risk of being branded “anti-American,” “anti-semite” or “conspiracy theorist.”

Truth is an inconvenience for government and for the interest groups whose campaign contributions control government.

Truth is an inconvenience for prosecutors who want convictions, not the discovery of innocence or guilt.

Truth is inconvenient for ideologues.

Today many whose goal once was the discovery of truth are now paid handsomely to hide it. “Free market economists” are paid to sell offshoring to the American people. High-productivity, high value-added American jobs are denigrated as dirty, old industrial jobs. Relicts from long ago, we are best shed of them. Their place has been taken by “the New Economy,” a mythical economy that allegedly consists of high-tech white collar jobs in which Americans innovate and finance activities that occur offshore. All Americans need in order to participate in this “new economy” are finance degrees from Ivy League universities, and then they will work on Wall Street at million dollar jobs.

Economists who were once respectable took money to contribute to this myth of “the New Economy.”

And not only economists sell their souls for filthy lucre. Recently we have had reports of medical doctors who, for money, have published in peer-reviewed journals concocted “studies” that hype this or that new medicine produced by pharmaceutical companies that paid for the “studies.”

The Council of Europe is investigating the drug companies’ role in hyping a false swine flu pandemic in order to gain billions of dollars in sales of the vaccine.

The media helped the US military hype its recent Marja offensive in Afghanistan, describing Marja as a city of 80,000 under Taliban control. It turns out that Marja is not urban but a collection of village farms.

And there is the global warming scandal, in which NGOs. the UN, and the nuclear industry colluded in concocting a doomsday scenario in order to create profit in pollution.

Wherever one looks, truth has fallen to money.

Wherever money is insufficient to bury the truth, ignorance, propaganda, and short memories finish the job.

I remember when, following CIA director William Colby’s testimony before the Church Committee in the mid-1970s, presidents Gerald Ford and Ronald Reagan issued executive orders preventing the CIA and U.S. black-op groups from assassinating foreign leaders. In 2010 the US Congress was told by Dennis Blair, head of national intelligence, that the US now assassinates its own citizens in addition to foreign leaders.

When Blair told the House Intelligence Committee that US citizens no longer needed to be arrested, charged, tried, and convicted of a capital crime, just murdered on suspicion alone of being a “threat,” he wasn’t impeached. No investigation pursued. Nothing happened. There was no Church Committee. In the mid-1970s the CIA got into trouble for plots to kill Castro. Today it is American citizens who are on the hit list. Whatever objections there might be don’t carry any weight. No one in government is in any trouble over the assassination of U.S. citizens by the U.S. government.

As an economist, I am astonished that the American economics profession has no awareness whatsoever that the U.S. economy has been destroyed by the offshoring of U.S. GDP to overseas countries. U.S. corporations, in pursuit of absolute advantage or lowest labor costs and maximum CEO “performance bonuses,” have moved the production of goods and services marketed to Americans to China, India, and elsewhere abroad. When I read economists describe offshoring as free trade based on comparative advantage, I realize that there is no intelligence or integrity in the American economics profession.

Intelligence and integrity have been purchased by money. The transnational or global U.S. corporations pay multi-million dollar compensation packages to top managers, who achieve these “performance awards” by replacing U.S. labor with foreign labor. While Washington worries about “the Muslim threat,” Wall Street, U.S. corporations and “free market” shills destroy the U.S. economy and the prospects of tens of millions of Americans.

Americans, or most of them, have proved to be putty in the hands of the police state.

Americans have bought into the government’s claim that security requires the suspension of civil liberties and accountable government. Astonishingly, Americans, or most of them, believe that civil liberties, such as habeas corpus and due process, protect “terrorists,” and not themselves. Many also believe that the Constitution is a tired old document that prevents government from exercising the kind of police state powers necessary to keep Americans safe and free.

Most Americans are unlikely to hear from anyone who would tell them any different.

I was associate editor and columnist for the Wall Street Journal. I was Business Week’s first outside columnist, a position I held for 15 years. I was columnist for a decade for Scripps Howard News Service, carried in 300 newspapers. I was a columnist for the Washington Times and for newspapers in France and Italy and for a magazine in Germany. I was a contributor to the New York Times and a regular feature in the Los Angeles Times. Today I cannot publish in, or appear on, the American “mainstream media.”

For the last six years I have been banned from the “mainstream media.” My last column in the New York Times appeared in January, 2004, coauthored with Democratic U.S. Senator Charles Schumer representing New York. We addressed the offshoring of U.S. jobs. Our op-ed article produced a conference at the Brookings Institution in Washington, D.C. and live coverage by C-Span. A debate was launched. No such thing could happen today.

For years I was a mainstay at the Washington Times, producing credibility for the Moony newspaper as a Business Week columnist, former Wall Street Journal editor, and former Assistant Secretary of the U.S. Treasury. But when I began criticizing Bush’s wars of aggression, the order came down to Mary Lou Forbes to cancel my column.

The American corporate media does not serve the truth. It serves the government and the interest groups that empower the government.

America’s fate was sealed when the public and the anti-war movement bought the government’s 9/11 conspiracy theory. The government’s account of 9/11 is contradicted by much evidence. Nevertheless, this defining event of our time, which has launched the US on interminable wars of aggression and a domestic police state, is a taboo topic for investigation in the media. It is pointless to complain of war and a police state when one accepts the premise upon which they are based.

These trillion dollar wars have created financing problems for Washington’s deficits and threaten the U.S. dollar’s role as world reserve currency. The wars and the pressure that the budget deficits put on the dollar’s value have put Social Security and Medicare on the chopping block. Former Goldman Sachs chairman and U.S. Treasury Secretary Hank Paulson is after these protections for the elderly. Fed chairman Bernanke is also after them. The Republicans are after them as well. These protections are called “entitlements” as if they are some sort of welfare that people have not paid for in payroll taxes all their working lives.

With over 21 per cent unemployment as measured by the methodology of 1980, with American jobs, GDP, and technology having been given to China and India, with war being Washington’s greatest commitment, with the dollar over-burdened with debt, with civil liberty sacrificed to the “war on terror,” the liberty and prosperity of the American people have been thrown into the trash bin of history.

The militarism of the U.S. and Israeli states, and Wall Street and corporate greed, will now run their course. As the pen is censored and its might extinguished, I am signing off.

Paul Craig Roberts was an editor of the Wall Street Journal and an Assistant Secretary of the U.S. Treasury. His latest book, HOW THE ECONOMY WAS LOST, has just been published by CounterPunch/AK Press. He can be reached at: PaulCraigRoberts@yahoo.com

Monday, March 29, 2010

dietary news and other links

I'm going to start w some dietary studies today-

http://www.medscape.com/viewarticle/719056?src=mpnews&spon=17&uac=99331SV

Reduce both carbohydrate and saturated fat intake, for healthiest diet, or

http://www.medscape.com/viewarticle/718893?src=mpnews&spon=17&uac=99331SV

Drink orange juice w your sausage McBiscuit, or Bangers and Mash for the Brits. I like the sound of the OJ option better.

http://mp.medscape.com/cgi-bin1/DM/y/hCwvO0SWHqx0Dyp0K5UL0Ed&uac=99331SV

US infants are Vit D deficient. As the father of an infant, this one was relevant, at least to me.

************************************************************************

And now back to politics-

Here is a good article on alleged teaparty racism in toward Black Caucus members. I too am sceptical of the charges leveled, and the "stunt" by these congessman that may have lead to these accusations.

http://whiskeyandgunpowder.com/do-they-wear-white-hoods-at-their-tea-parties/

If you haven't seen my previous post re: left wing anti-semitism, check it out here-http://drg-freeassociation.blogspot.com/2010/03/leftist-anti-semitism.html

*********************************************************************

Here is a rather long article about the significance/insignificance of the Greece situation, being one of many straws on the camel's back. I mainly link to this story because of its reference to a book I really enjoyed a few years back, which I highly recommend, by Mark Buchanan called Ubiquity, Why Catastrophes Happen.

You can skip either to pg 4 or the bottom of pg 2- http://www.frontlinethoughts.com/pdf/mwo032610.pdf

Friday, March 26, 2010

To prepare for the new healthcare reform package, the White House felt it necessary to develop a new medical symbol that truly depicts the Health Care Plan you will be getting.

Below commentaries and links shamelessly stolen from Ed Steer's Gold and Silver Daily

"Social Security to See Payout Exceed Pay-In This Year"... "This important threshold was not expected to crossed until at least 2016, according to the Congressional Budget Office. "Analysts have long tried to predict the year when Social Security would pay out more than it took in because they view it as a tipping point — the first step of a long, slow march to insolvency." The link to the story is here.

more banking malfeasance

One of the most interesting stories to come out of yesterday's hearings was this "Deep Throat" trader out of London that I mentioned briefly yesterday. He warned the CFTC in a series of e-mails about an upcoming decline in the silver market that JPMorgan instigated. He wanted to speak at the CFTC hearings, but was denied. The series of e-mails he sent to the CFTC is contained in a GATA dispatch bearing the headline "A London trader walks the CFTC through a silver manipulation in advance". What's in these e-mails should be no surprise to anyone... as it pretty much describes what both Ted Butler and GATA have been saying for years about the actual process itself... and you've certainly seen me talk about it in this column on many occasions as well. Now we have solid confirmation that this is all true. This is a must read... and the link is here.

********************************************************************************

Poll for Kit Bond's US senate replacement, I support libertarian Jonathon Dine, vote here.

****************************************************************************

Save the Economy by Hiding From the Census

By Vedran Vuk

In a recent Census Bureau press release, one statistic really stands out, mailing back the census form costs the government 42 cents while sending someone to check non-responses costs $56. At first, my reaction was to immediately mail back my census form. With all the government spending going on, there is no need for more waste.

But then, I remembered the Census’s own rhetoric. If I perform my civic duty of filling out the Census, my community will get more money. This sounds great doesn’t it?

But, if I want more money for my community, then why should I return the form through the mail? Think about it. Imagine if everyone in my community, the Baltimore metropolitan area, refused to mail their census forms back.

The number of census takers that would be hired to count the 2.7 million people in the metropolitan area would be enormous. Baltimore would get a gigantic economic stimulus. According to the Census, there are 2.59 people living in the average household – that’s over 1.04 million households in the area. Multiply this number by $56 to get $58.4 million from the Census jobs stimulus.

But wait, good citizen. Don’t stop there. A real patriot doesn’t comply with the Census. The $56 assumes an average number of repeat visits per residence. If everyone hides in the back room for the first couple of visits, maybe we can push that average to $100 dollars per household. Wouldn’t it be great! We’d have a $104 million stimulus in just months.

Unfortunately, there’s a big problem with my comical idea and the Census’s own marketing campaign rhetoric. Although the Census promises to allocate more money to our communities as a result of filling out the forms, it doesn’t make much sense. The Census isn’t some well-meaning philanthropist distributing money for the good of the people. Neither are the temporary census jobs a free lunch.

All the money is either taxed or borrowed by the government – the ultimate payer is always us. If everyone in the U.S. refused to mail back the forms and hid from the Census to jack up payrolls, the country would not be better off. In fact, it would be a very silly exercise. Sadly, every government stimulus is founded on the same illogical idea as the Census’s own promises. One man’s stimulus is always another man’s tax. On net, there is no economic improvement.

Further, the Bureau’s marketing campaign disguises a very political perspective. It assumes that government programs always benefit the community. But, what if some government programs actually make it worse?

For example, welfare has been and always will be a hot topic in this country. According to a study by the Census Bureau, for 2007, Census data was used to help redistribute $16.5 billion in TANF funds, commonly known as welfare. If you’re on the left, more welfare payments mean a good thing for the community. However, someone on the right could see welfare as fueling dependency and ingraining long term poverty.

Some effects of government spending clearly don’t improve anything and others are debatable. If America wants to get back on its feet economically, we must pay attention to the foundations that made us stand tall in the first place rather than temporary government stimulus. The foundations of America weren’t built by paper pushers at the motor vehicles administration and census takers. Private enterprise through technological innovations, world class companies, and entrepreneurship – big and small – empowered America.

Yet, every stimulus program brings us closer and closer to a world opposite of those foundations. If we continue down our current route, sooner or later, we’ll have more people working at regulatory government agencies than the regulated industries themselves. The Department of Agriculture is much like this already – it grows bigger and bigger though the number of actual farmers grows smaller and smaller.

Our history isn’t hard to decipher. We didn’t acquire the greatest nation status through trillion dollar stimulus plans. The U.S. needs change, but not the usual proposed spending and waste. We need change back to the basics by encouraging growth in the private sector, not the public one.

Before I sign off, I see that the dollar is rallying (the dollar index is at its highest level since late May of last year) on more bad news from the eurozone as Fitch Ratings cut Portugal’s credit grade. There’s going to be a lot more bad news coming out of Europe in the months ahead and the euro will likely be knocked down some more, so expect the dollar to fare fairly well in the very short-term. But do keep in mind that all fiat currencies eventually fall to their intrinsic value – zero.

Below commentaries and links shamelessly stolen from Ed Steer's Gold and Silver Daily

"Social Security to See Payout Exceed Pay-In This Year"... "This important threshold was not expected to crossed until at least 2016, according to the Congressional Budget Office. "Analysts have long tried to predict the year when Social Security would pay out more than it took in because they view it as a tipping point — the first step of a long, slow march to insolvency." The link to the story is here.

more banking malfeasance

One of the most interesting stories to come out of yesterday's hearings was this "Deep Throat" trader out of London that I mentioned briefly yesterday. He warned the CFTC in a series of e-mails about an upcoming decline in the silver market that JPMorgan instigated. He wanted to speak at the CFTC hearings, but was denied. The series of e-mails he sent to the CFTC is contained in a GATA dispatch bearing the headline "A London trader walks the CFTC through a silver manipulation in advance". What's in these e-mails should be no surprise to anyone... as it pretty much describes what both Ted Butler and GATA have been saying for years about the actual process itself... and you've certainly seen me talk about it in this column on many occasions as well. Now we have solid confirmation that this is all true. This is a must read... and the link is here.

********************************************************************************

Poll for Kit Bond's US senate replacement, I support libertarian Jonathon Dine, vote here.

****************************************************************************

Save the Economy by Hiding From the Census

By Vedran Vuk

In a recent Census Bureau press release, one statistic really stands out, mailing back the census form costs the government 42 cents while sending someone to check non-responses costs $56. At first, my reaction was to immediately mail back my census form. With all the government spending going on, there is no need for more waste.

But then, I remembered the Census’s own rhetoric. If I perform my civic duty of filling out the Census, my community will get more money. This sounds great doesn’t it?

But, if I want more money for my community, then why should I return the form through the mail? Think about it. Imagine if everyone in my community, the Baltimore metropolitan area, refused to mail their census forms back.

The number of census takers that would be hired to count the 2.7 million people in the metropolitan area would be enormous. Baltimore would get a gigantic economic stimulus. According to the Census, there are 2.59 people living in the average household – that’s over 1.04 million households in the area. Multiply this number by $56 to get $58.4 million from the Census jobs stimulus.

But wait, good citizen. Don’t stop there. A real patriot doesn’t comply with the Census. The $56 assumes an average number of repeat visits per residence. If everyone hides in the back room for the first couple of visits, maybe we can push that average to $100 dollars per household. Wouldn’t it be great! We’d have a $104 million stimulus in just months.

Unfortunately, there’s a big problem with my comical idea and the Census’s own marketing campaign rhetoric. Although the Census promises to allocate more money to our communities as a result of filling out the forms, it doesn’t make much sense. The Census isn’t some well-meaning philanthropist distributing money for the good of the people. Neither are the temporary census jobs a free lunch.

All the money is either taxed or borrowed by the government – the ultimate payer is always us. If everyone in the U.S. refused to mail back the forms and hid from the Census to jack up payrolls, the country would not be better off. In fact, it would be a very silly exercise. Sadly, every government stimulus is founded on the same illogical idea as the Census’s own promises. One man’s stimulus is always another man’s tax. On net, there is no economic improvement.

Further, the Bureau’s marketing campaign disguises a very political perspective. It assumes that government programs always benefit the community. But, what if some government programs actually make it worse?

For example, welfare has been and always will be a hot topic in this country. According to a study by the Census Bureau, for 2007, Census data was used to help redistribute $16.5 billion in TANF funds, commonly known as welfare. If you’re on the left, more welfare payments mean a good thing for the community. However, someone on the right could see welfare as fueling dependency and ingraining long term poverty.

Some effects of government spending clearly don’t improve anything and others are debatable. If America wants to get back on its feet economically, we must pay attention to the foundations that made us stand tall in the first place rather than temporary government stimulus. The foundations of America weren’t built by paper pushers at the motor vehicles administration and census takers. Private enterprise through technological innovations, world class companies, and entrepreneurship – big and small – empowered America.

Yet, every stimulus program brings us closer and closer to a world opposite of those foundations. If we continue down our current route, sooner or later, we’ll have more people working at regulatory government agencies than the regulated industries themselves. The Department of Agriculture is much like this already – it grows bigger and bigger though the number of actual farmers grows smaller and smaller.

Our history isn’t hard to decipher. We didn’t acquire the greatest nation status through trillion dollar stimulus plans. The U.S. needs change, but not the usual proposed spending and waste. We need change back to the basics by encouraging growth in the private sector, not the public one.

Before I sign off, I see that the dollar is rallying (the dollar index is at its highest level since late May of last year) on more bad news from the eurozone as Fitch Ratings cut Portugal’s credit grade. There’s going to be a lot more bad news coming out of Europe in the months ahead and the euro will likely be knocked down some more, so expect the dollar to fare fairly well in the very short-term. But do keep in mind that all fiat currencies eventually fall to their intrinsic value – zero.

Thursday, March 25, 2010

http://www.caseyresearch.com/displayCdd.php?id=379 If you skip down to the end of this publication, the article, Privatizing Gains, Socializing Losses, and Demonizing Wall Street, raises some interesting points regarding bailouts which I had not thought of before- esp. "Why are we so against bailouts that help taxpaying individuals, when the current system bails out non-productive indivuals on a daily basis." I don't like any bailouts (e.g.welfare), and certainly any tax-payer dollars going toward wall street bonuses. If you are against bailouts, you should read this short article.

Old friend Spencer Rogers sent me the following article, Health bill included big Republican idea: individual mandate- http://www.miamiherald.com/2010/03/24/1545524/individual-health-insurance-mandate.html. I've been meaning to write specifically about the individual mandate, and now is as good a time as any. While the concept may have started as a "republican" or "conservative" idea, it is now intellectually lazy or dishonest to characterize it as such. "Big Drug company" or "Big insurance company" friendly would be much more appropriate. The Dem's (esp head cheerleader Obama) have at the end of this HCR fight, painted this as a fight for the little guy against big business, drawing on a clearly Populist theme. This certainly has some traction, especially among their dwindling political base. In fact, the individual mandate makes this bill very friendly for both Big Pharma and Big Insurance. "What, what, WHAT?" some of you may be asking?

This provision adds millions of previously uninsured people to the positive side of the ledger for these large companies, w their new subsidized, mandated, drug consumption and insurance premium purchases. Any revenue loss from price caps will be made up for by increased market penetration, Business 101. This was probably a backroom deal. The trick was to fool the American Public into thinking that these big businesses were actually against the plan. (It actually didn't work all that well). The took a page out of the bankers playbook from the turn of last century. Big Pharma/Insurance PRETENDED, to be against the bill and didn't fight either the righteous criticisms of their industries or the misleading rhetoric, knowing that the legislation would be beneficial to them. If the sheeple thought industry was against it, it must be good for the sheeple was the logic.

This was the tactic used by the banking industry, to gain passage of the Federal Reserve Act in 1913. Act like Banking didn't want it. Who didn't want to stick it to JP Morgan and Phillip Rothschild? They must have been laughing all the way to the bank (home). They've been sticking it to us ever since. (for more on this read, "The Creature from Jekyll Island. A Brief History of the Federal Reserve")

Don't get me wrong, there are clearly big problems in the Healthcare system as it is. However, the recently passed legislation solves few and creates many more, and will cost a bundle.

***************************************************************************

I would also like to point out that the mainstream media, while gleefully reporting threats and acts of violence against organizations and congressmen supporting the HCR bill, I have heard little about attacks on those against the bill which I have to find here- http://www.weaselzippers.net/blog/2010/03/republican-rep-receives-threat-for-voting-no-on-obamacare-threatens-to-shoot-teabaggers.html and http://www.weaselzippers.net/blog/2010/03/antiabortion-group-flooded-with-threats-and-hateful-messages-following-health-care-vote.html

Leftist Anti-Semitism

I'm stealing this from http://www.weaselzippers.net/blog/, I thought the pictures and descriptions should be widely diseminated. Why does the mainstream media ignore racism, when it comes from the left? I support their freedom of speech, but I reserve the right criticize their distasteful ideas and presentation.

*****************************************************************************

Leftist Anti-Semitism on Full Display During Anti-War Parade in Hollywood...

And yet the left along with their MSM allies breathlessly claim there's rampant racism at Tea-Party rallies, where they're lucky to find one kook who tries to makes everyone look bad, at lefty gatherings it's blatant and in-your-face...

The Annual March of the Moonbats - March 20, 2010- Ringo's Pictures

*****************************************************************************

Leftist Anti-Semitism on Full Display During Anti-War Parade in Hollywood...

And yet the left along with their MSM allies breathlessly claim there's rampant racism at Tea-Party rallies, where they're lucky to find one kook who tries to makes everyone look bad, at lefty gatherings it's blatant and in-your-face...

The Annual March of the Moonbats - March 20, 2010- Ringo's Pictures

Wednesday, March 24, 2010

mostly gold, a little healthcare

http://www.caseyresearch.com/displayCdd.php?id=378. Skip to the second part of this article, "Help! I’ve Been Taxed and I Can’t Get Up" to read about the massive tax increases required to pay for healthcare- not just on the rich.

I frequently borrow (steal) heavily from Ed Steer (see Gold and silver links). His piece today was important enough, despite being a bit esoteric that I copied a large portion. If you invest in PMs, his column should be a daily read.

European Central Bank reported that "gold and gold receivables" rose by a million Euros last week... "attributed to a purchase of gold coin by one of the captive central banks. So far this year, two E1 million rises and one E1 million fall has been the extent of the ECB group [reported] gold activity."

Tomorrow is the day for the CFTC hearings into concentration and position limits by the CFTC in Washington. GATA's chairman Bill Murphy will be there to present the case on behalf of our organization. We should all wish him well, as there is much at stake. If you want to watch/listen to these hearings as they progress, all the information necessary to do that is contained in this GATA release, which secretary treasurer Chris Powell sent out yesterday. The link is http://www.gata.org/node/8455

First of all, when GATA started out, it took us a couple of years for us to figure out that it wasn't just a few bullion banks like JPMorgan and Goldman Sachs out to make a few bucks... but that it was a conspiracy on a far grander scale which involved the U.S. Treasury Department and the Federal Reserve... plus other central banks. It was the cornerstone of Secretary Treasurer Robert Rubin's "strong dollar policy" which we still hear talk of every once in a while.

With that policy now in the trash bin of history, the price management scheme is still going on... with the two U.S. bullion banks [at least the ones we can see]... JPMorgan and HSBC USA... doing the heavy lifting for the Fed and the Treasury Department. These are two of the big bullion banks in the Commercial '4 or less' traders category of the Commitment of Traders report. Now they are stuck with these huge short positions which cannot be covered without driving the prices of both metals to the outer edges of the know universe.

Gold and silver, the two monetary metals, are the often mentioned "canaries in the coal mine". A parabolic rise in the face of the economic, financial and monetary woes that this planet is currently experiencing, would cause a stampede out of paper assets and into hard assets... a fight that they are [slowly, but surely] losing anyway. They're trying to prevent 'death by a single thrust'... by substituting 'death by a thousand cuts' instead. It's a controlled retreat... and they're hoping that nobody will notice... that's why they have their 'talking heads' that they trot out to denigrate gold whenever the precious metals markets are showing... or about to show... too much 'irrational exuberance'.

But what brought GATA's fight into clear focus, was a piece written by British economist Peter Warburton back in April of 2001. The whole article, entitled "The debasement of world currency: it is inflation, but not as we know it" is worth reading

http://www.gold-eagle.com/gold_digest_01/warburton041801.html... but it's three paragraphs from that essay that brings the Federal Reserve's fight against the precious metals [and all physical commodities] to the forefront. I've quoted them in my column before, but on the eve of the CFTC hearings tomorrow, they are worth revisiting... and here they are. Don't forget Warburton wrote this nine years ago next month... so some of the figures he's using are out of date... but that doesn't matter.

Central banks are engaged in a desperate battle on two fronts

"What we see at present is a battle between the central banks and the collapse of the financial system fought on two fronts. On one front, the central banks preside over the creation of additional liquidity for the financial system in order to hold back the tide of debt defaults that would otherwise occur. On the other, they incite investment banks and other willing parties to bet against a rise in the prices of gold, oil, base metals, soft commodities or anything else that might be deemed an indicator of inherent value. Their objective is to deprive the independent observer of any reliable benchmark against which to measure the eroding value, not only of the US dollar, but of all fiat currencies. Equally, their actions seek to deny the investor the opportunity to hedge against the fragility of the financial system by switching into a freely traded market for non-financial assets."

"It is important to recognize that the central banks have found the battle on the second front much easier to fight than the first. Last November, I estimated the size of the gross stock of global debt instruments at $90 trillion for mid-2000. How much capital would it take to control the combined gold, oil and commodity markets? Probably, no more than $200bn, using derivatives. Moreover, it is not necessary for the central banks to fight the battle themselves, although central bank gold sales and gold leasing have certainly contributed to the cause. Most of the world’s large investment banks have over-traded their capital [bases] so flagrantly that if the central banks were to lose the fight on the first front, then their stock would be worthless. Because their fate is intertwined with that of the central banks, investment banks are willing participants in the battle against rising gold, oil and commodity prices."

"Central banks, and particularly the US Federal Reserve, are deploying their heavy artillery in the battle against a systemic collapse. This has been their primary concern for at least seven years. Their immediate objectives are to prevent the private sector bond market from closing its doors to new or refinancing borrowers and to forestall a technical break in the Dow Jones Industrials. Keeping the bond markets open is absolutely vital at a time when corporate profitability is on the ropes. Keeping the equity index on an even keel is essential to protect the wealth of the household sector and to maintain the expectation of future gains. For as long as these objectives can be achieved, the value of the US dollar can also be stabilized in relation to other currencies, despite the extraordinary imbalances in external trade."

There, in a nutshell, is the entire story.

So, with that preamble out of the way, I now present today's 8-page letter sent to CFTC chairman Gary Gensler, by GATA director Adrian Douglas. It goes without saying that this a must read... and if you have the time, you should read it more than once. This letter, and the letter sent in by GATA chairman Bill Murphy, pretty much sum up what GATA's presentation tomorrow in Washington is all about.

Borrowing heavily from the work of silver analyst Ted Butler and others, Adrian spells it out. There are too many highlights to mention them all, but one of the biggest is the graph from German researcher and GATA consultant Dimitri Speck at the top of page 4... which is titled "Average GOLD Intraday change: August 1993 - March 2009". That's five and a half years of data. How many times, dear reader, have I mentioned the fact that the lows of the day [in both metals] occurs at the London p.m. gold fix? Well, this graph says it all. There's also a fine example of it in both gold and silver in the two graphs at the top of today's column. The red line is Monday, March 22nd... the lows of the day, you ask... in New York trading at the London p.m. gold fix.

Mr. Douglas also commented on something else that's a favourite whipping boy of mine... and that's the fact that the two U.S. bullion banks holding the biggest short positions in silver and gold... JPMorgan and HSBC USA... also happen to be the custodians for the SLV and GLD ETFs. I've mentioned that countless times in this column over the years. At GATA's Annual General Meeting in Vancouver, B.C. in January... board member Catherine Austin Fitts brought up the subject of a "material omission" in the prospectuses of these two ETFs regarding this... and I'm glad to see that Adrian has put this very important issue on the record with the CFTC. GATA plans to proceed further on this point once tomorrow's CFTC hearing is out the way.

There are many other solid points made by Douglas in this letter... and as I said before, I urge you to give this letter the time it deserves. It's headlined "Comments for the Commission for the Public Hearing on the Metals Market: March 25, 2010"... and the link to the pdf file is here.https://marketforceanalysis.com/index_assets/CFTC%20HEARING%20ON%20METALS%20MARKETS.pdf

I frequently borrow (steal) heavily from Ed Steer (see Gold and silver links). His piece today was important enough, despite being a bit esoteric that I copied a large portion. If you invest in PMs, his column should be a daily read.

European Central Bank reported that "gold and gold receivables" rose by a million Euros last week... "attributed to a purchase of gold coin by one of the captive central banks. So far this year, two E1 million rises and one E1 million fall has been the extent of the ECB group [reported] gold activity."

Tomorrow is the day for the CFTC hearings into concentration and position limits by the CFTC in Washington. GATA's chairman Bill Murphy will be there to present the case on behalf of our organization. We should all wish him well, as there is much at stake. If you want to watch/listen to these hearings as they progress, all the information necessary to do that is contained in this GATA release, which secretary treasurer Chris Powell sent out yesterday. The link is http://www.gata.org/node/8455

First of all, when GATA started out, it took us a couple of years for us to figure out that it wasn't just a few bullion banks like JPMorgan and Goldman Sachs out to make a few bucks... but that it was a conspiracy on a far grander scale which involved the U.S. Treasury Department and the Federal Reserve... plus other central banks. It was the cornerstone of Secretary Treasurer Robert Rubin's "strong dollar policy" which we still hear talk of every once in a while.

With that policy now in the trash bin of history, the price management scheme is still going on... with the two U.S. bullion banks [at least the ones we can see]... JPMorgan and HSBC USA... doing the heavy lifting for the Fed and the Treasury Department. These are two of the big bullion banks in the Commercial '4 or less' traders category of the Commitment of Traders report. Now they are stuck with these huge short positions which cannot be covered without driving the prices of both metals to the outer edges of the know universe.

Gold and silver, the two monetary metals, are the often mentioned "canaries in the coal mine". A parabolic rise in the face of the economic, financial and monetary woes that this planet is currently experiencing, would cause a stampede out of paper assets and into hard assets... a fight that they are [slowly, but surely] losing anyway. They're trying to prevent 'death by a single thrust'... by substituting 'death by a thousand cuts' instead. It's a controlled retreat... and they're hoping that nobody will notice... that's why they have their 'talking heads' that they trot out to denigrate gold whenever the precious metals markets are showing... or about to show... too much 'irrational exuberance'.

But what brought GATA's fight into clear focus, was a piece written by British economist Peter Warburton back in April of 2001. The whole article, entitled "The debasement of world currency: it is inflation, but not as we know it" is worth reading

http://www.gold-eagle.com/gold_digest_01/warburton041801.html... but it's three paragraphs from that essay that brings the Federal Reserve's fight against the precious metals [and all physical commodities] to the forefront. I've quoted them in my column before, but on the eve of the CFTC hearings tomorrow, they are worth revisiting... and here they are. Don't forget Warburton wrote this nine years ago next month... so some of the figures he's using are out of date... but that doesn't matter.

Central banks are engaged in a desperate battle on two fronts

"What we see at present is a battle between the central banks and the collapse of the financial system fought on two fronts. On one front, the central banks preside over the creation of additional liquidity for the financial system in order to hold back the tide of debt defaults that would otherwise occur. On the other, they incite investment banks and other willing parties to bet against a rise in the prices of gold, oil, base metals, soft commodities or anything else that might be deemed an indicator of inherent value. Their objective is to deprive the independent observer of any reliable benchmark against which to measure the eroding value, not only of the US dollar, but of all fiat currencies. Equally, their actions seek to deny the investor the opportunity to hedge against the fragility of the financial system by switching into a freely traded market for non-financial assets."

"It is important to recognize that the central banks have found the battle on the second front much easier to fight than the first. Last November, I estimated the size of the gross stock of global debt instruments at $90 trillion for mid-2000. How much capital would it take to control the combined gold, oil and commodity markets? Probably, no more than $200bn, using derivatives. Moreover, it is not necessary for the central banks to fight the battle themselves, although central bank gold sales and gold leasing have certainly contributed to the cause. Most of the world’s large investment banks have over-traded their capital [bases] so flagrantly that if the central banks were to lose the fight on the first front, then their stock would be worthless. Because their fate is intertwined with that of the central banks, investment banks are willing participants in the battle against rising gold, oil and commodity prices."

"Central banks, and particularly the US Federal Reserve, are deploying their heavy artillery in the battle against a systemic collapse. This has been their primary concern for at least seven years. Their immediate objectives are to prevent the private sector bond market from closing its doors to new or refinancing borrowers and to forestall a technical break in the Dow Jones Industrials. Keeping the bond markets open is absolutely vital at a time when corporate profitability is on the ropes. Keeping the equity index on an even keel is essential to protect the wealth of the household sector and to maintain the expectation of future gains. For as long as these objectives can be achieved, the value of the US dollar can also be stabilized in relation to other currencies, despite the extraordinary imbalances in external trade."

There, in a nutshell, is the entire story.

So, with that preamble out of the way, I now present today's 8-page letter sent to CFTC chairman Gary Gensler, by GATA director Adrian Douglas. It goes without saying that this a must read... and if you have the time, you should read it more than once. This letter, and the letter sent in by GATA chairman Bill Murphy, pretty much sum up what GATA's presentation tomorrow in Washington is all about.

Borrowing heavily from the work of silver analyst Ted Butler and others, Adrian spells it out. There are too many highlights to mention them all, but one of the biggest is the graph from German researcher and GATA consultant Dimitri Speck at the top of page 4... which is titled "Average GOLD Intraday change: August 1993 - March 2009". That's five and a half years of data. How many times, dear reader, have I mentioned the fact that the lows of the day [in both metals] occurs at the London p.m. gold fix? Well, this graph says it all. There's also a fine example of it in both gold and silver in the two graphs at the top of today's column. The red line is Monday, March 22nd... the lows of the day, you ask... in New York trading at the London p.m. gold fix.

Mr. Douglas also commented on something else that's a favourite whipping boy of mine... and that's the fact that the two U.S. bullion banks holding the biggest short positions in silver and gold... JPMorgan and HSBC USA... also happen to be the custodians for the SLV and GLD ETFs. I've mentioned that countless times in this column over the years. At GATA's Annual General Meeting in Vancouver, B.C. in January... board member Catherine Austin Fitts brought up the subject of a "material omission" in the prospectuses of these two ETFs regarding this... and I'm glad to see that Adrian has put this very important issue on the record with the CFTC. GATA plans to proceed further on this point once tomorrow's CFTC hearing is out the way.

There are many other solid points made by Douglas in this letter... and as I said before, I urge you to give this letter the time it deserves. It's headlined "Comments for the Commission for the Public Hearing on the Metals Market: March 25, 2010"... and the link to the pdf file is here.https://marketforceanalysis.com/index_assets/CFTC%20HEARING%20ON%20METALS%20MARKETS.pdf

Tuesday, March 23, 2010

todays links

I guess there are some good things about socialist countries. Maybe we can learn something about how to deal with corrupt financial officials. "North Korean finance chief executed for botched currency reform"

******************************************************************************